BACK TO NORMAL

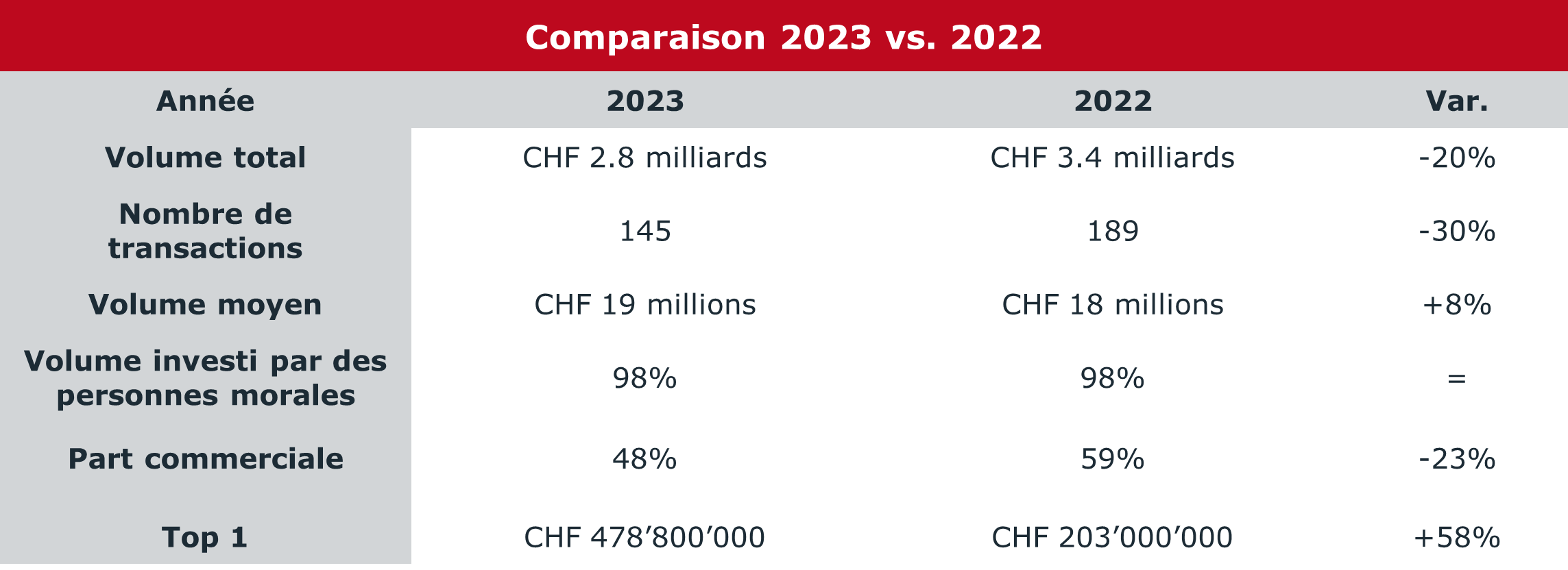

After three consecutive years above the CHF 3 billion mark, the Geneva investment property market paused in 2023, with an annual investment volume of around CHF 2.8 billion, down 20% compared with 2022.

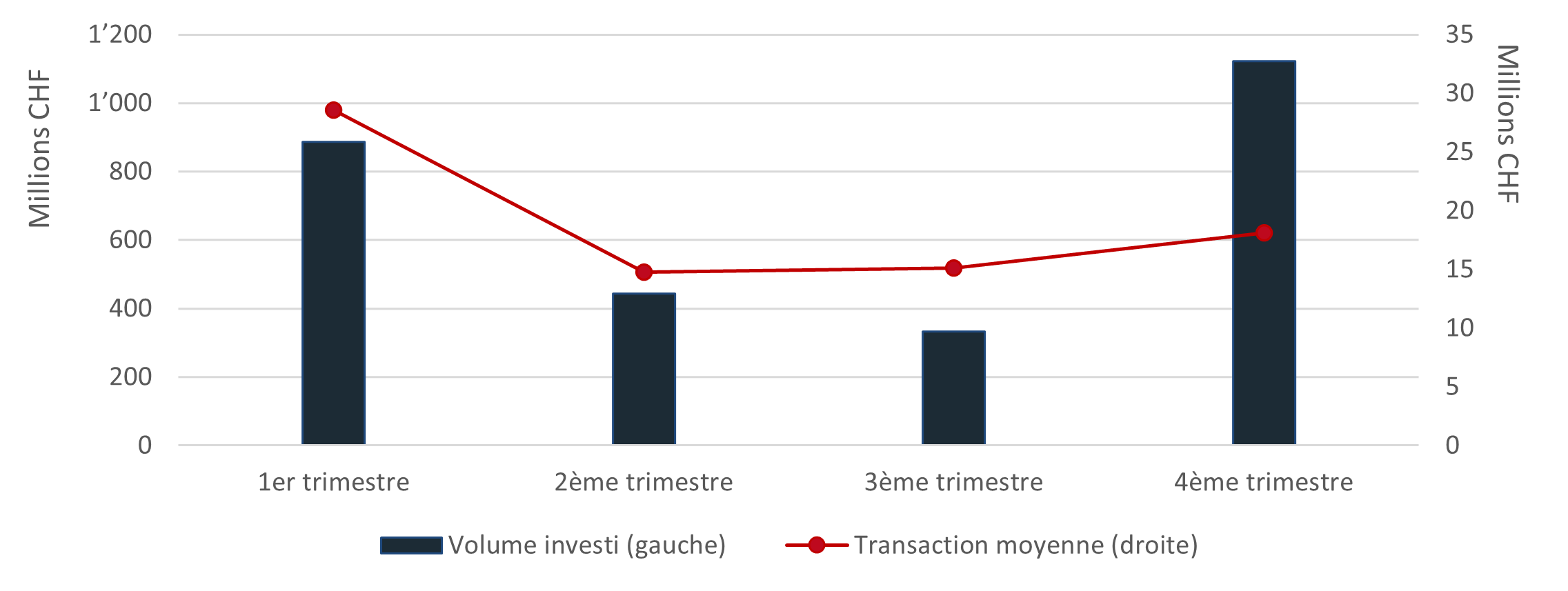

In 2023, the Swiss National Bank (SNB) continued the monetary policy it had initiated in mid-2022 to combat inflation, implementing further increases in its key policy rate, which reached 1.75% by year-end. In this economic environment, the Geneva investment property market was logically less dynamic and recorded a decline of around 30% in the number of transactions over the year. We note in particular that the second and third quarters of 2023 were especially quiet, with less than CHF 800 million invested over this period, representing only 28% of total annual volume. Fortunately, the year-end sprint did materialise: the fourth quarter alone captured around 40% of the invested volume and approximately 43% of the total number of transactions.

Another key feature of 2023 is that investment in commercial real estate accounted for only about 48% of total volume, compared with 59% in 2022. This trend reflects a certain investor wariness towards this asset class, particularly office buildings, whose rental markets are currently facing significant challenges in major global economic capitals. Investors therefore favoured residential properties which, in a context of housing shortage and rising rents, continue to see their rental income grow.

TOP 5 TRANSACTIONS

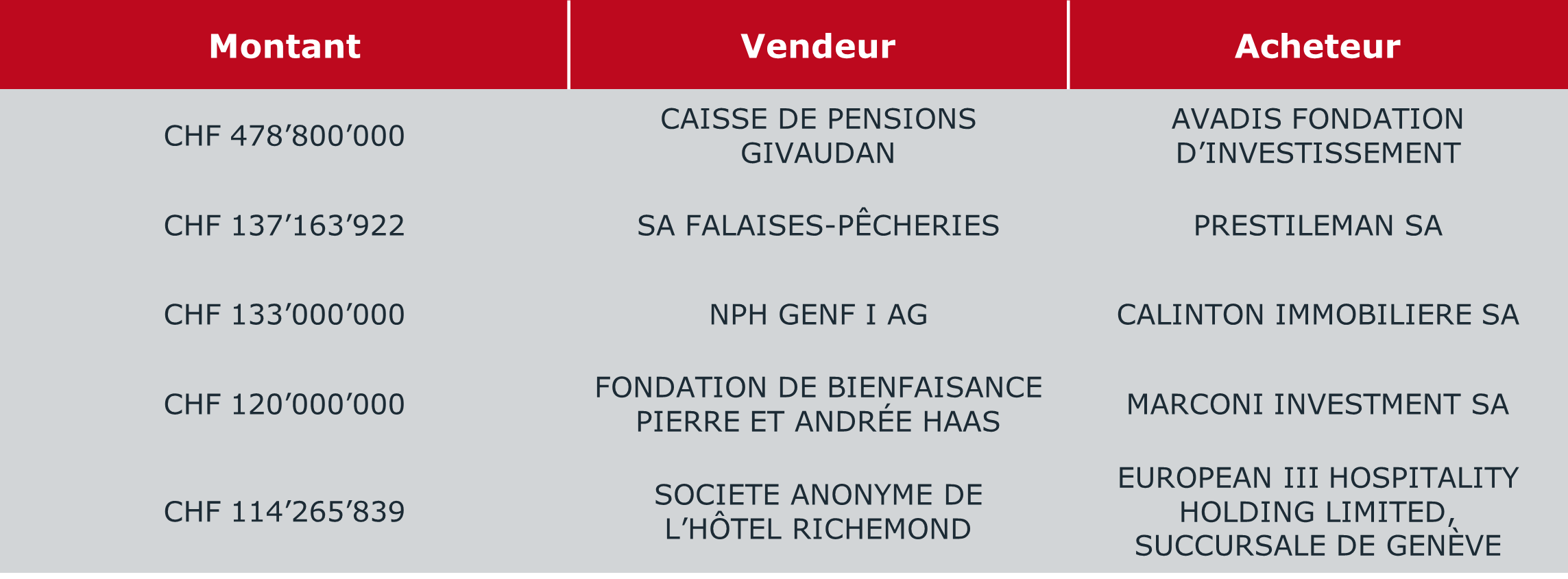

The five largest transactions alone accounted for 37% of total invested volume, compared with 24% in 2022. The largest, for approximately CHF 479 million, concerned the acquisition of a portfolio of 16 residential buildings by the Avadis pension foundation from the Givaudan pension fund. There were also two transactions on Rue du Rhône – a symbol of Geneva’s “prime” segment – for a total of CHF 253 million (Calinton Immobilière SA and Marconi Investment SA).

INSTITUTIONAL INVESTORS CONTINUE TO INVEST BUT ALSO REBALANCE THEIR PORTFOLIOS

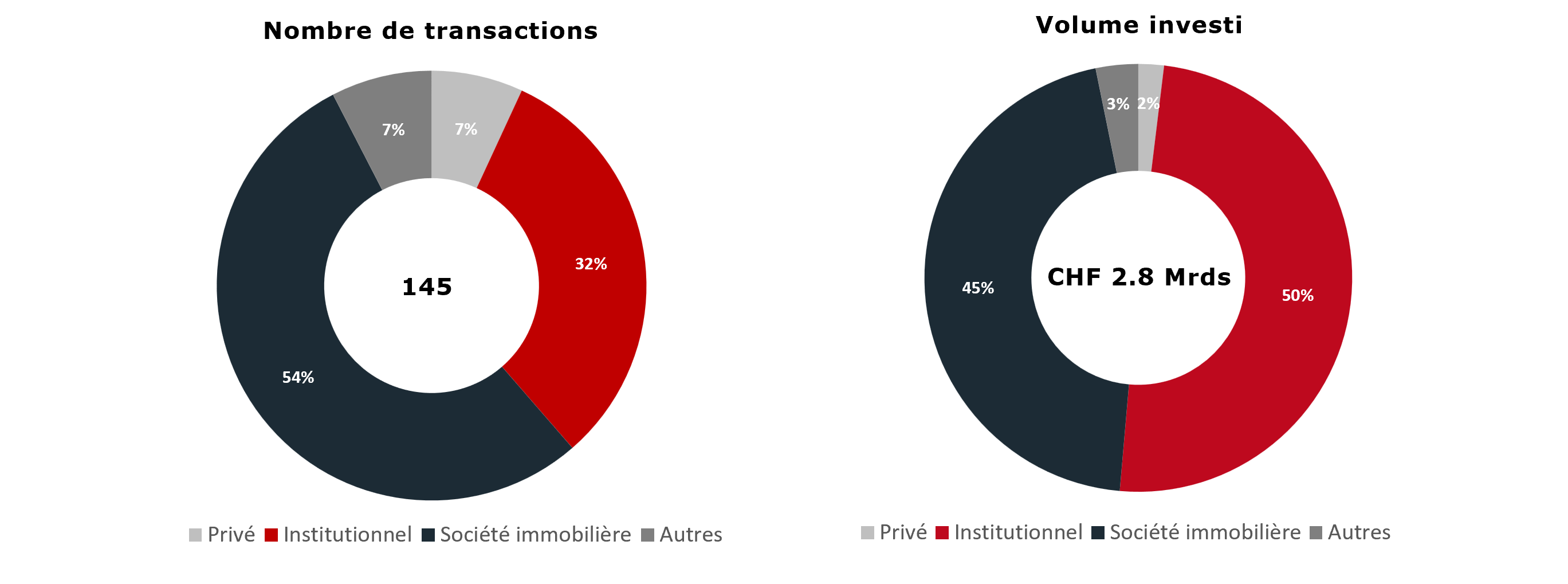

In terms of number of transactions, real estate companies represent the largest buyer category, with around 54% (left-hand chart). The reduction in 2020 of the corporate tax rate in the Canton of Geneva from 24.16% to 13.99% has revitalised this investment vehicle, which is popular among private investors as it offers both tax advantages and discretion.

In terms of invested volume (right-hand chart), institutional investors rank first, accounting for almost 50% of total volume, with an average transaction size of around CHF 30 million for this buyer category. Far behind, private investors represent barely 2% of invested volume, with an average deal size of around CHF 5.4 million.

In opposition to recent years, institutional investors were also the main sellers in 2023, with around 32% of total volume. In terms of number of sales, private investors remain well ahead, accounting for 54% of disposals.

AVERAGE GROSS YIELD AND PRICE PER SQUARE METRE

For this market study, we sought to estimate the average gross yield of completed transactions. To do so, we used several AI-based applications that enabled us to compile various data useful for estimating probable lettable areas and market rents. This allowed us to determine the potential rent rolls of residential and mixed-use buildings. As the results for commercial buildings did not appear sufficiently reliable, we excluded them from our analysis.

By combining our results with the sale prices published in the FAO and filtering out extreme values, we were able to determine an average gross yield of 4.31% on approximately CHF 1.45 billion invested in residential and mixed-use properties.

OUR ANALYSIS

In a market searching for direction throughout 2023, our team had the opportunity to run several sale processes in Geneva, enabling us to closely observe and analyse investor behaviour.

First, we noted a gradual withdrawal over the year by certain investors, particularly insurance companies, which had until recently been regarded as the strongest buyers in the market. This shift created room for pension funds and investment foundations to move into the spotlight.

We also observed an opportunistic approach from real estate funds. In a challenging environment for indirect real estate, these funds were very active as sellers, but the strongest among them also continued to buy properties, taking advantage of the price correction.

Finally, although sustainability has been a factor in investment strategies for more than a decade, we found that it is now becoming the – almost primary – decision-making criterion. The better a property scores on sustainability metrics, the higher the price investors are willing to pay.

The SNB’s first interest rate cut on 21 March 2024, together with forecasts of further reductions, suggests that the market will be more dynamic in 2024. However, we are convinced that investors’ “selective” behaviour in favour of sustainable buildings will only intensify over the coming years.

Note: Only transactions above CHF 2 million published in the FAO are included in the annual transaction volume. In addition, land transactions are not included.