SUMMARY

- 157 transactions involving investment buildings recorded

- Total transaction volume of CHF 2.5 billion (vs. 2.8 billion in 2023)

- Average transaction size of CHF 16 million (vs. 19 million in 2023)

- Key rate cuts leading to an acceleration of the market in the second half of 2024

- Significant institutional capital available following numerous capital raises (over CHF 4.5 billion in 2024)

- Institutional investors focused on new or well-maintained residential properties, but limited supply on the market

- Commercial assets – particularly office buildings – are in low demand outside city centres (19% of transaction volume vs. 48% in 2023)

- In our view, the market is now on a clearly upward trend

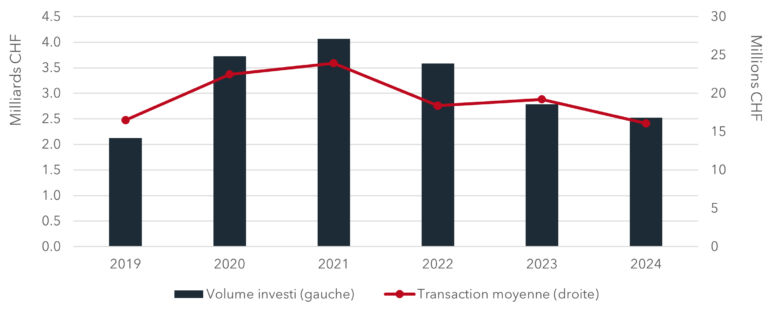

DEVELOPMENT 2019–2024

Sources: FAO Genève.

NB: Only buildings with a transaction value above CHF 2 million published in the FAO are included in the annual transaction volume. In addition, land transactions are not included. are not included.

PICK-UP IN ACTIVITY FROM THE SECOND HALF OF THE YEAR

In 2024, a total volume of approximately CHF 2.52 billion was invested in the Canton of Geneva, representing a 9% decline compared with 2023. Over the year, 157 transactions were recorded, an increase of 8% versus 2023.

The average transaction size stands at around CHF 16 million, down from the previous two years (CHF 19 million in 2023 and CHF 18 million in 2022).

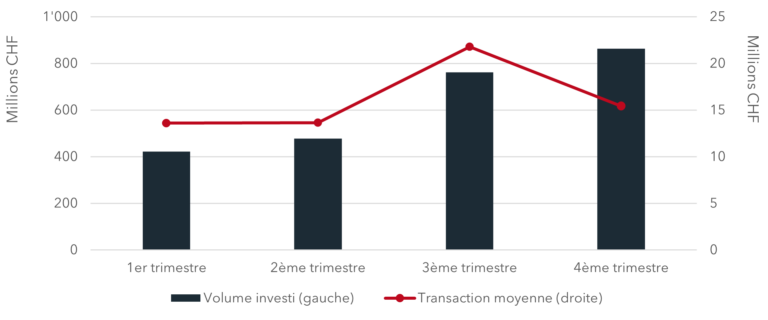

In response to slowing inflation, the Swiss National Bank (SNB) sent a strong signal in terms of monetary policy. Four cuts in the key interest rate were implemented during the year, bringing it down to 0.5% (now 0.25%). Despite this, the first half remained relatively subdued, with approximately CHF 900 million invested – 36% of the annual volume – and 66 transactions completed. By contrast, the second half was significantly more dynamic, with around CHF 1.60 billion invested – 64% of the annual volume – and 91 transactions.

The most striking feature of the year is the very low share invested in commercial buildings: just 19% of total volume, i.e. less than CHF 500 million. By comparison, this share stood at 62% in 2022 and 48% in 2023. This asset class was clearly neglected by the market in 2024, with the exception of a few opportunistic investors.

Investors favoured the acquisition of residential buildings, which accounted for 60% of total volume, or more than CHF 1.5 billion. Despite lower yields and tighter regulation, residential assets still offer lower rental risk, with the vacancy rate for rental housing in the Canton of Geneva currently at 0.5%.

2024 BY QUARTER

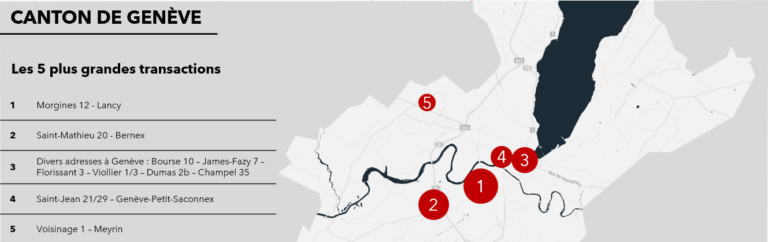

TOP 5 TRANSACTIONS

The five largest transactions accounted for 20% of the total invested volume, compared with 37% in 2023 and 24% in 2022. The largest, amounting to approximately CHF 112 million, concerned the acquisition of an office building by Investis Properties from one of UBS’s funds. Two of the top-five transactions were transfers between vehicles within insurance companies. Notably, no major transaction was recorded in Geneva’s CBD.

GROSS ENTRY YIELD FOR RESIDENTIAL BUILDINGS

For this study, our objective was to reflect market entry yields for residential buildings. To this end, we identified all transactions in which a real estate fund was involved, either as buyer or as seller.

Real estate funds are required to publish certain information in their semi-annual and annual reports, including rental income for their properties and details of acquisitions and disposals during the period.

We identified 16 transactions involving at least one real estate fund. These represent a volume of approximately CHF 471 million, or 32% of the total volume invested in residential buildings.

This analysis results in an average gross entry yield of 3.98% for residential buildings. It is worth noting that the prime gross entry yield stands at 3.22% for a building located in the Plainpalais district, sold by a Swiss Life real estate fund to a real estate company.

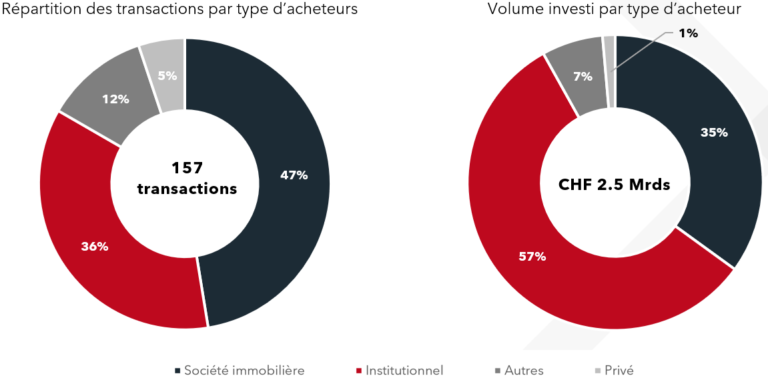

A MARKET STILL DRIVEN BY REAL ESTATE COMPANIES AND INSTITUTIONAL INVESTORS

In terms of number of transactions, real estate companies are the most active buyer type, accounting for around 47% of completed deals (left-hand chart).

In terms of invested volume (right-hand chart), institutional investors are in the lead with 57% of total volume and an average transaction size of around CHF 25 million. They are followed by real estate companies with 35% of total volume and an average deal size of approximately CHF 12 million. Far behind, private investors account for just 1.4% of total invested volume, with an average transaction size of around CHF 4.3 million.

As in the previous year, institutional investors were also the main sellers in 2024, with around 38% of total volume. This trend is part of an asset rotation strategy by certain real estate funds seeking to divest non-strategic properties. Lastly, private investors continue to be the main sellers in terms of number of transactions, with 51% of sales, representing a total of 79 deals.

OUR ANALYSIS

The five rate cuts implemented in 2024 and 2025 by the SNB, bringing the key rate down to 0.25%, have cemented a favourable environment for real estate investors. In this context, we observed a clear acceleration in the second half of the year, both in terms of transaction volume and especially in terms of demand from institutional investors.

Indeed, more than CHF 4.5 billion was raised by various real estate vehicles in 2024, and by the end of February 2025 there were 19 ongoing capital increases targeting CHF 2.2 billion in total, including a very large operation by UBS Swiss Sima aiming to raise CHF 350 million. These funds must be allocated to the direct real estate market, resulting in substantial liquidity in the system.

At present, acquisition strategies are heavily concentrated on residential real estate, primarily recent or new buildings offering high energy performance. Unfortunately, such assets are scarce on the market, particularly as construction activity has slowed considerably in recent years.

In the absence of “perfect” properties and in a highly competitive environment, investors will likely have to turn to other options if they wish to deploy their capital – notably residential buildings requiring renovation and offering rental upside, as well as commercial properties which now provide more attractive yields and more flexible regulatory constraints.

We believe that the bottom of the market is now behind us and we expect 2025 to be a very dynamic year in terms of transactions.